How To Start A Business In 15 Steps: Guide, Checklist, And Canvas

You’re ready to take the leap and start a business. Congratulations! Making that decision might feel risky, but it’s a good thing.

In fact, 74% of small and medium business owners are willing to take big risks to ensure they succeed. “Fortune,” as the saying goes, “favours the bold.”

Still, you should also consider …

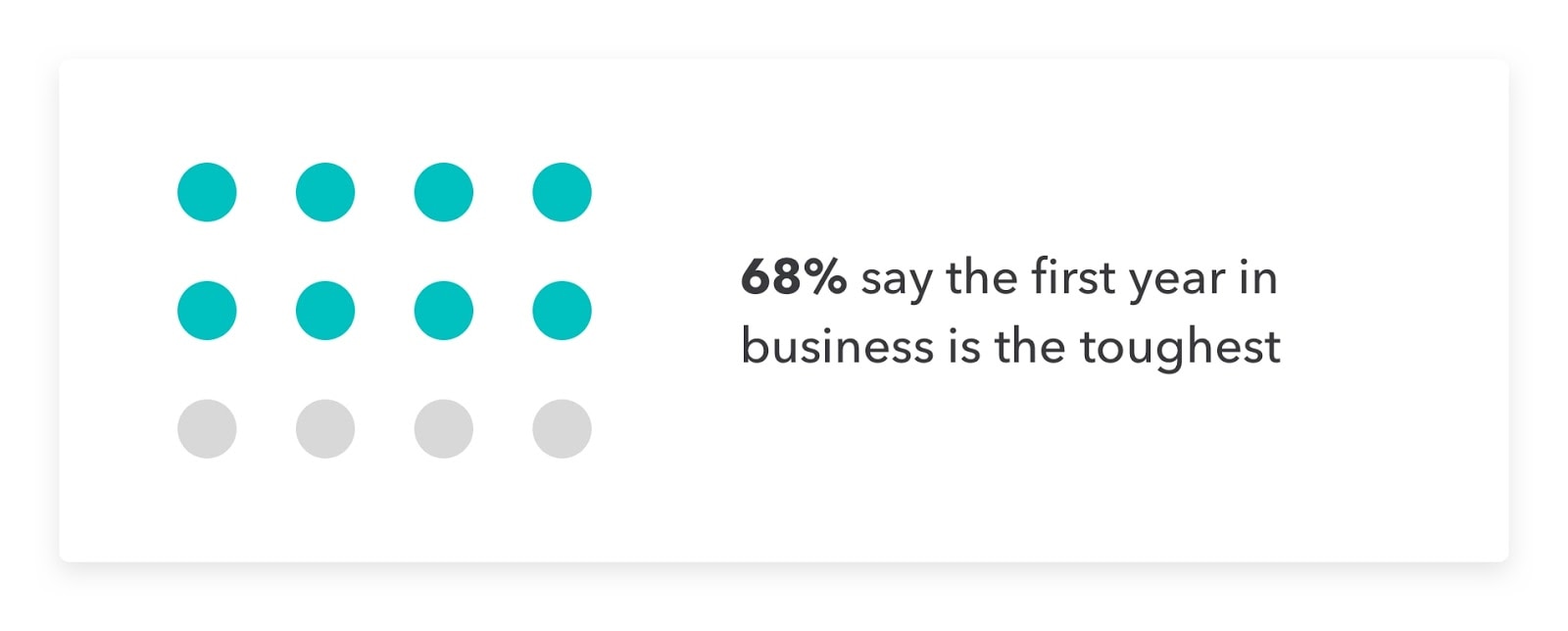

- Two-thirds say the first year is the toughest

- Half of small businesses survive five years or more

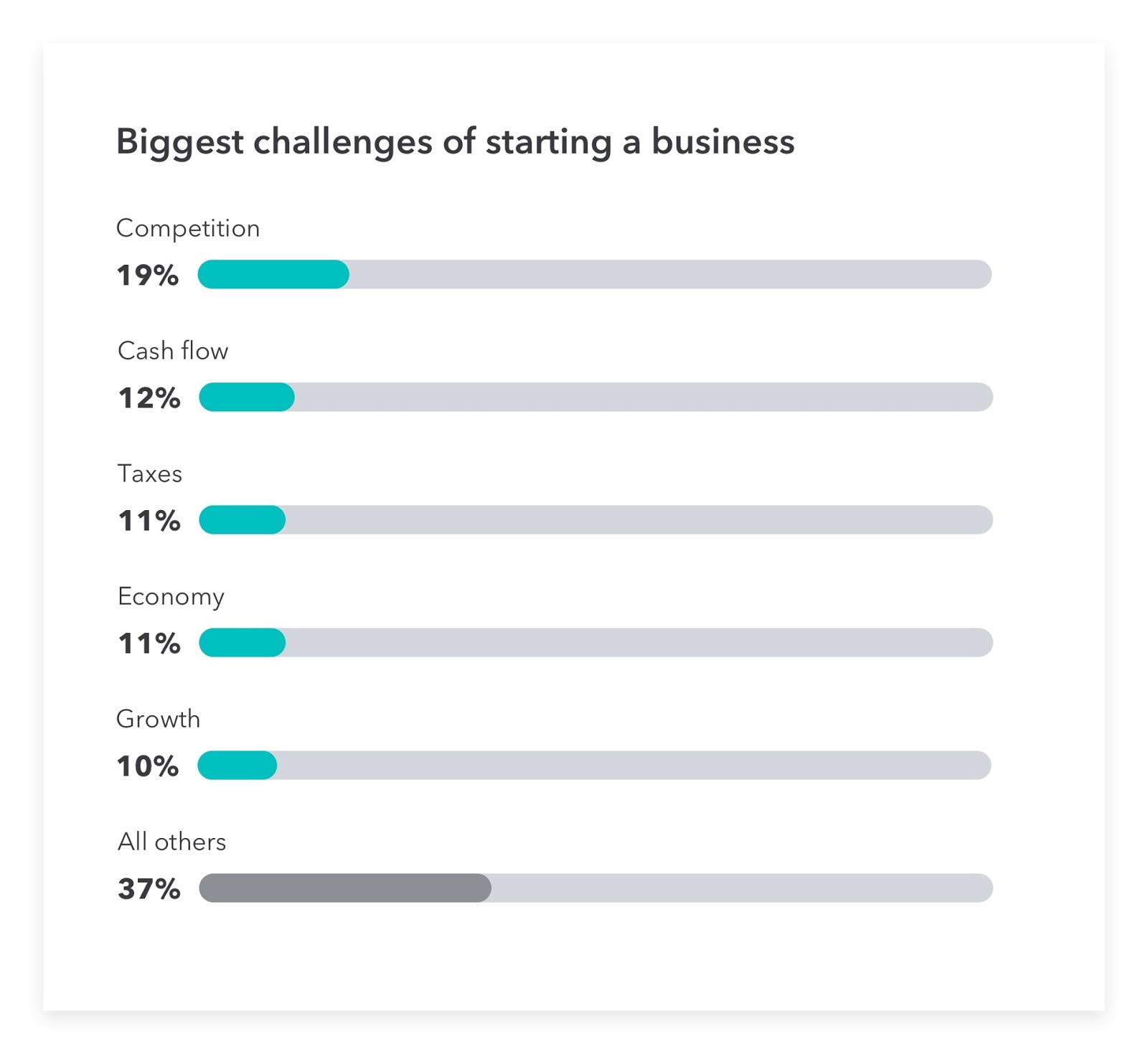

- Competition, cash flow, and taxes are the top three threat

Data from QuickBooks, TSheets (now QuickBooks Time), and Oxford Economics

Creating something all on your own is both rewarding and an opportunity to achieve work-life balance while pursuing your passions. But, it isn’t easy.

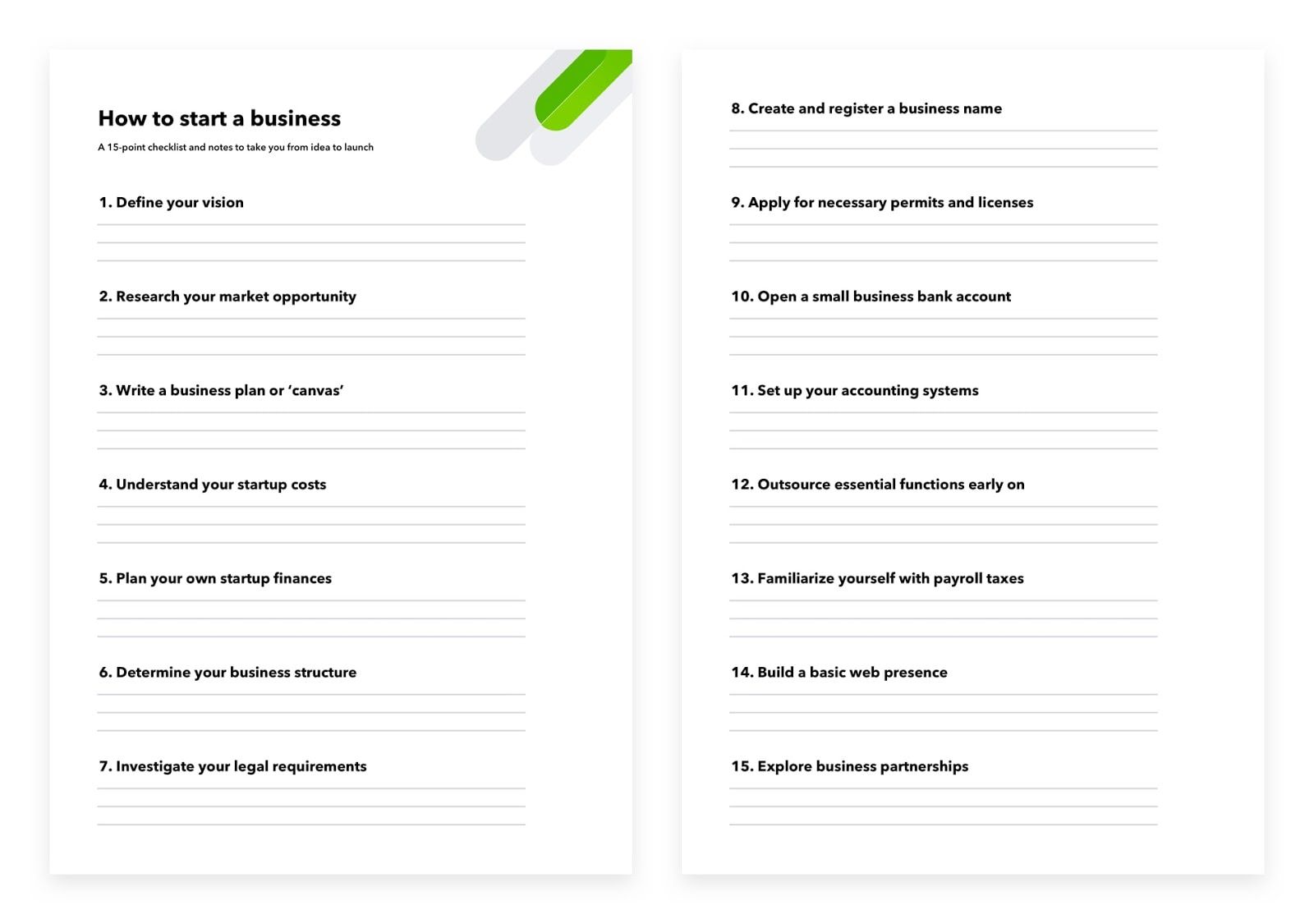

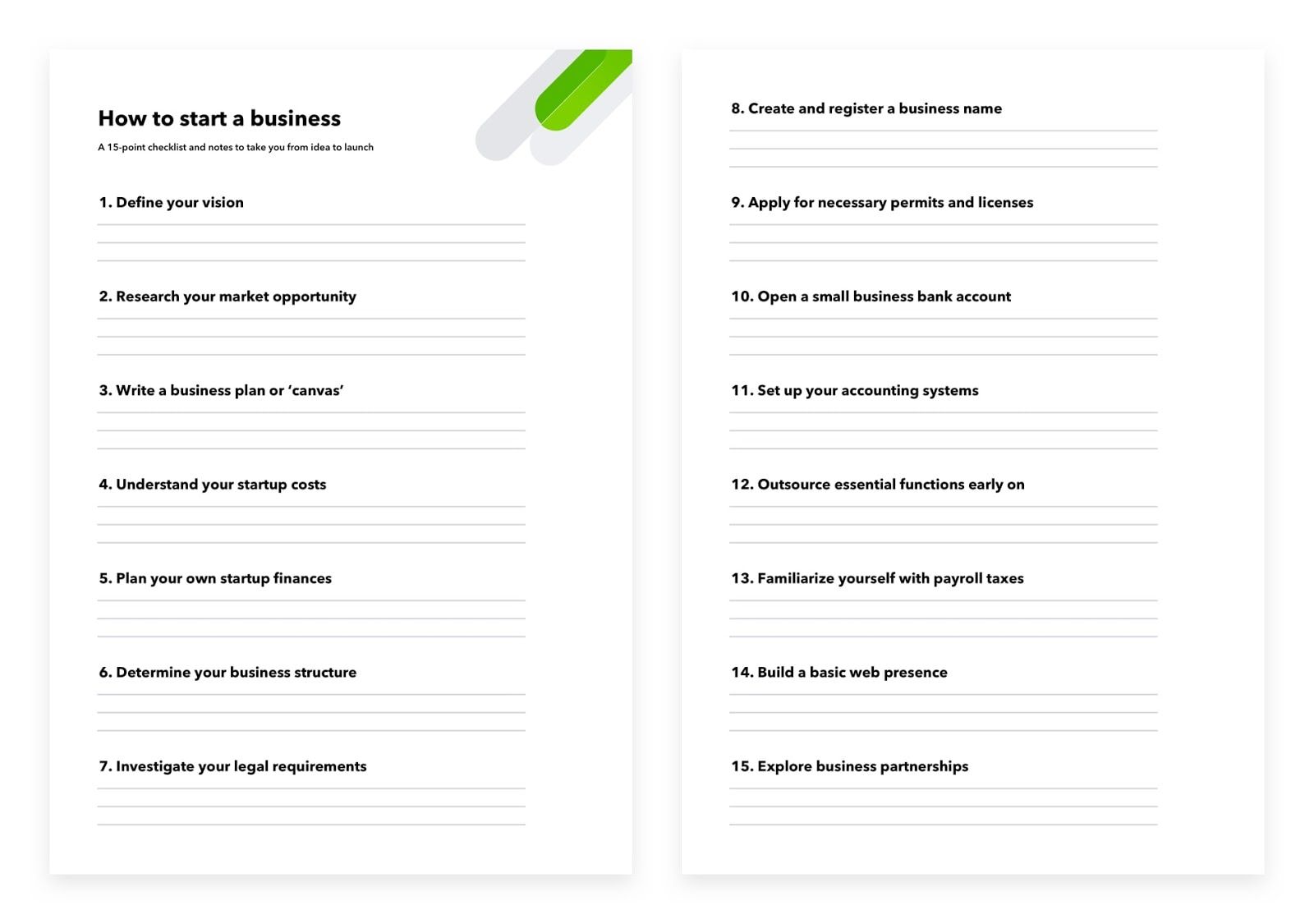

To help, this article guides you through the 15 steps to start a business along with a downloadable checklist you can fill out to go from idea to launch to success:

1. Define your vision

A business without a vision is like a ship without a rudder. You need to define it early on to set everything else into motion.

Writing a mission statement is a good idea to lay down this foundation. In a few paragraphs, identify your company goals and high-level strategy to accomplish them.

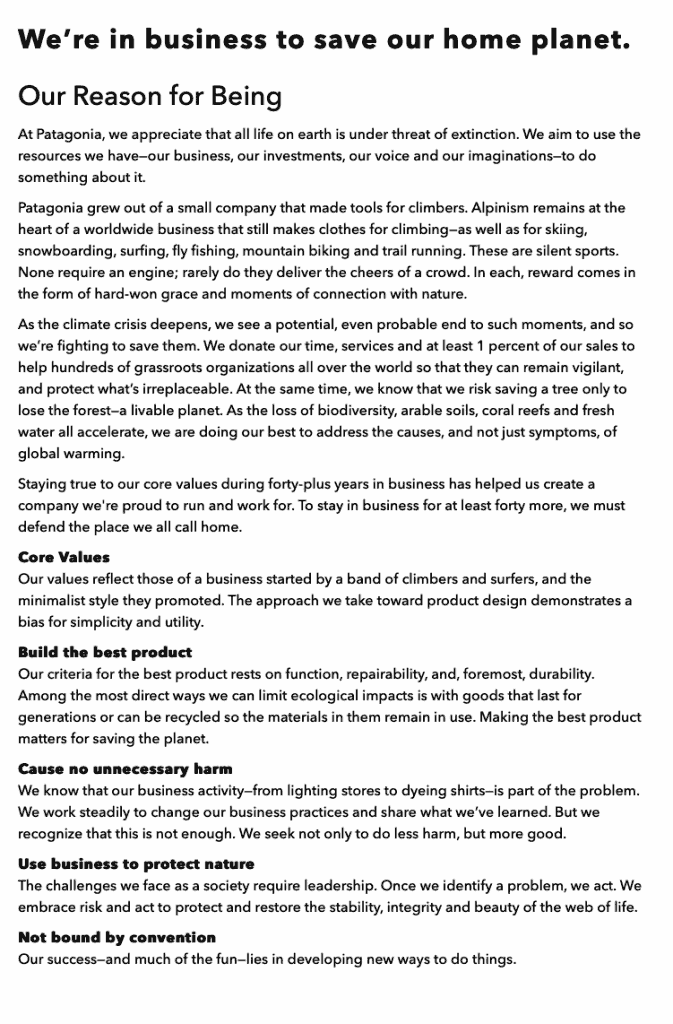

It’s helpful to visit some of your competitors’ websites to learn from and emulate what they’ve written. Patagonia’s mission statement inspires customers and employees alike:

Notice that it’s broken down into three parts you can likewise follow …

- Mission statement: “We’re in the business to save our home planet.”

- Narrative: “Our reason for being.”

- List: “Core values,” etc.

When writing out your vision, be as clear and to the point as you can be. Use the example above to write a powerful and motivational message to inspire team members to work together towards a common goal.

2. Research your market opportunity

There’s a lot to consider when starting a new business—everything from developing your product or service to accounting, legal, marketing, and more.

It’s easy to focus too much on small details before you see the big picture.

That’s why you should first validate that you have a strong business opportunity. Here are some critical steps to follow:

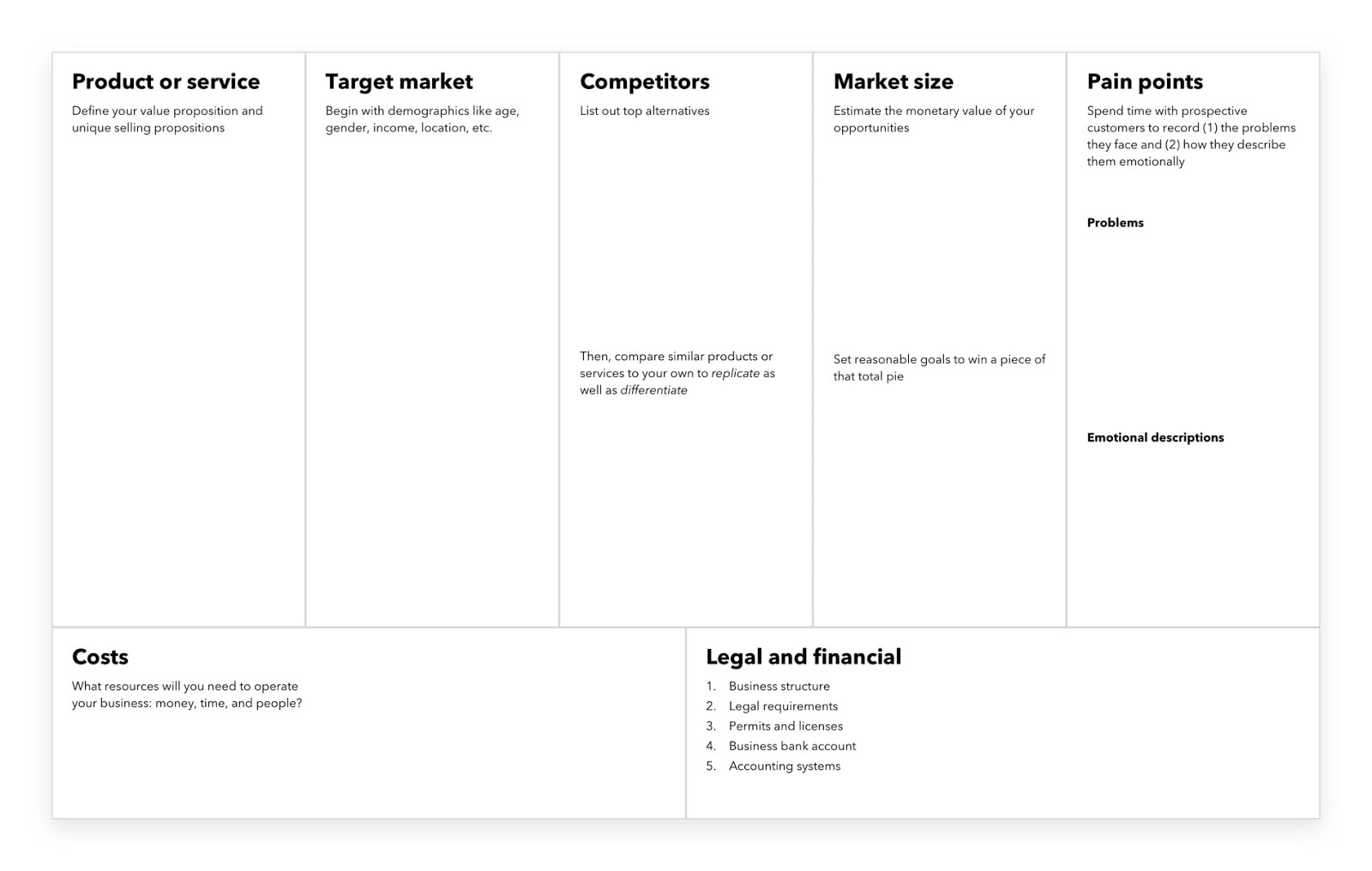

Select a product or service

It may sound obvious but what will your business sell and how do you plan to be different than competitors (e.g., what is your value proposition or unique selling proposition)?

Define your target market

Who will your business serve? Begin with demographics like age, gender, income, location, etc. Then, go deeper through personas or a customer journey map.

Identify key competitors

Having competition is a good thing. It means there’s demand. Compare similar products or services to your own, both to replicate what your market loves and differentiate.

Know your market size or opportunity

In the end, market research means quantifying the opportunity your product or service represents. Estimating the current and future monetary value of your business idea and setting reasonable goals for how you will win a piece of that pie.

But how? That brings us to our next step …

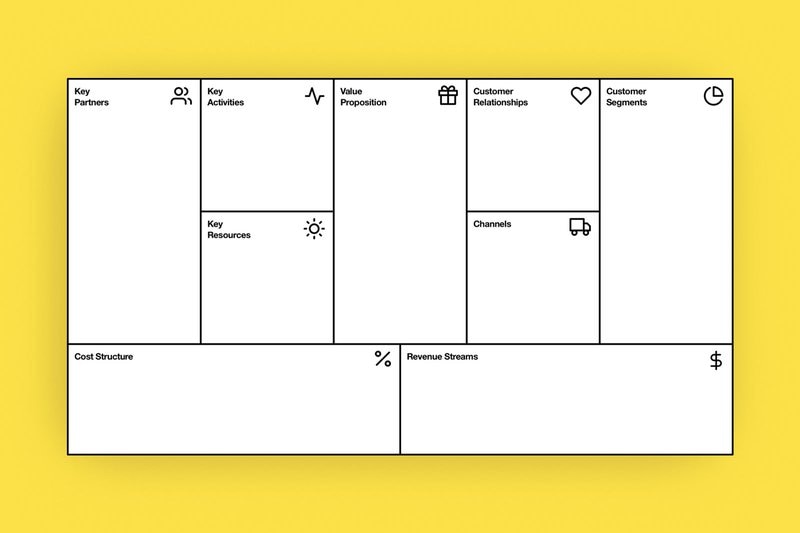

3. Write a business ‘canvas’ (then, a plan)

The good news is you’ve already done some of the work by tackling the first steps above. Keep in mind, your first business plan isn’t finite. Parts of it will most likely change as you learn more about your market and grow.

Some experts even say you should instead start with a business model canvas: a one-page document that covers the critical information you need to get started. This option will save you time and get you up and running faster.

Once you’ve been in business for a while, or you’re ready to seek funding, then you can build out a more detailed plan. It should cover each section in the screenshot above in more depth—everything from:

- Resources to operate

- Your overall marketing plan

- What your cost and sales structure will look like

- How you’ll manage your finances, expansion, and more

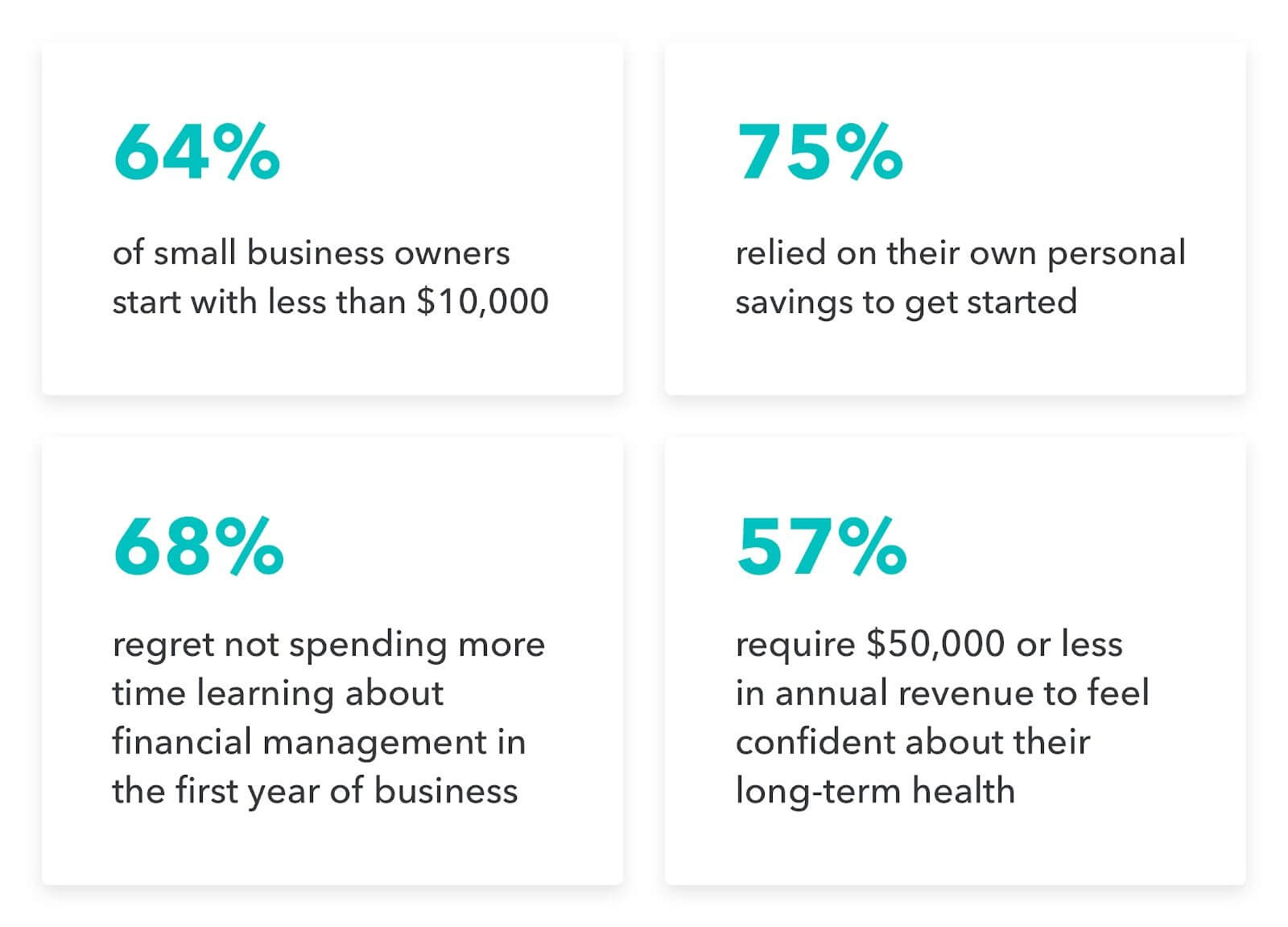

4. Understand your startup costs

Even if you’re self-funded, you must still understand your startup costs. Here are some important facts:

- The majority start with less than $10,000

- The number one regret of owners looking back on the first year is that they didn’t spend more time learning about financial management

- The majority require $50,000 or less in annual revenue to feel confident about their long-term health

You should start by mapping out all of the costs you anticipate having in the next year. Then, determine how much money you need to earn every month to stay in business (e.g., your operating income and salary).

Keep in mind, it takes a few years to build up your revenue. That’s why being mindful of your costs and cash flow is so critical, which leads us to the next step.

5. Plan your own starting finances

Determine how you will fund your business if you don’t have your own startup cash. There are many options that don’t involve seeking angel investments or venture capital, which are often better suited:

Crowdfunding

You’ve likely heard of crowdfunding. This is a popular route for many new business owners. It works by seeking funds from a large number of people, rather than one major investor.

Microloans

These are small business loans, often less than $10,000, that you can apply for to get your business off the ground. You’ll have to research your microloans, depending on what country you live in, as there are many different services to choose from.

Personal loans

If you have a good credit rating, you can take out a personal loan, rather than a business loan. You can also borrow against credit cards or a personal line of credit. Just be aware of long-term interest and tax implications before you do so.

Grants

Depending on what country you live in, you may be eligible for grants to help you finance, either from your government or private organisations. Again, you’ll have to research what those grants are, whether you qualify, and how to apply.

Friends and family

Last, but not least, plenty of businesses get their start through the help of friends and families. Don’t be embarrassed to reach out. At the same time, take those pitches seriously by outlining all the work you’ve done through your canvas or plan.

6. Determine your business structure

Now, it’s time to define what type of company you plan to run: your business entity. Are you better off as a sole trader or proprietor? Do you have a partner? Do you plan to incorporate?

Each option has its advantages as well as associated tax reporting responsibilities and regulatory requirements.

Here are definitions of the most common structures:

Sole proprietor or sole trader

This is a popular option for anyone who doesn’t have a lot of liabilities (e.g., no employees or major investments) when they are first starting out. As your business grows, you may wish to incorporate at a later date.

Business partnership

If you are going into business with one or more partners, then you will need to register as a business partnership. Because each partner will have a stake, you must work with a lawyer and a tax professional to layout the type, terms, and tax implications of your partnership.

Incorporated business

Some notable benefits of incorporating your business are tax breaks and to avoid personal or financial liabilities if, say, someone sues your company. Due to upfront costs, many sole traders wait until they have earned enough funds and are at the right stage to incorporate.

There are several other options, depending on which country you live in. Speak with an accountant or financial advisor to determine which option best suits your needs today and in the future.

7. Investigate your legal requirements

Before you launch your business, consult with a lawyer to ensure you’ve considered all the legal requirements. Include legal fees in your financial planning as well. It’s important to have a good lawyer on-call to solve legal and contract disputes, and for advice before signing a new contract.

Here are some of the questions to ask, and services to request, from a lawyer:

- Should your name or logo be registered as a trademark?

- Do you need a patent, copyright, or intellectual property protection?

- Can they create standard contracts for negotiating with other businesses and vendors?

- What’s involved in a sole proprietorship, forming a partnership, or incorporating your business?

- What’s the process for sharing equity when seeking private investors?

Different laws apply to every type of business, product, or service. Every country and even region will have its own set of laws as well. Your local and federal government websites are an excellent place to begin your research about requirements.

You should also consult national consumer and privacy laws for collecting personal customer information.

8. Create and register a business name

After you’ve had a conversation with your accountant and lawyer, it’s time to register your name. The process will differ by country and even regionally. Do your homework to understand your local requirements.

First, ensure your name is available. The quickest way to find out is through an online search. Type your desired name into every major search engine. Check social media platforms such as Facebook, Instagram, and Twitter. Then, reference your state and national registries.

If you plan to conduct business in multiple countries, be sure to check for the name’s use in those countries. There are local government services you can use to double-check that the name isn’t owned by someone else. Again, you’ll need to conduct an online search to find each of those services, depending on where you’ll operate.

You should register the name (to make sure it’s accepted) before creating business cards, logos, websites, and more. It’ll save you stress and likely a major headache later. Again, registration sites differ based on which regions and countries.

Finally, if you decide to register your name as a trademark, you’ll need to do so at this point as well. Your lawyer can guide you through this process. Keep in mind, there are additional costs associated with every registration you do.

9. Apply for permits and business licenses

Visit your relevant government services website to find out whether any national or regional licenses are required.

While you’re at it, check to see whether you qualify for any tax deductions and credits. Many local governments design special credits to help small businesses grow faster.

You might also need a special business number if you’ll be collecting goods and services taxes. For example, GST applies in Australia. It’s associated with the amount of annual sales you bring in and the GST you pay on business expenses.

To apply, visit the appropriate government website. Your accountant can advise on any other tax-related applications you may need to complete. Again, it depends on where you live and what type of business you are operating.

10. Open a small business bank account

There are different types of business bank accounts and products that can help you save money and grow faster. As soon as you’re ready to start your business, arrange a meeting with a business banking specialist to determine which type of account is right for your business.

Cross-reference the bank’s advice on any savings bundles or special accounts you might need with your accountant.

If you’re planning an international business strategy and expect to generate a high volume of sales in those overseas markets, opening a bank account in that market makes even more sense. You’ll save money on bank transfer and currency exchange rate fees.

In addition, establishing a financial presence country-by-country will make it easier for your bookkeeper and accountant during tax season, as they’ll be able to see separate statements for country-specific revenue.

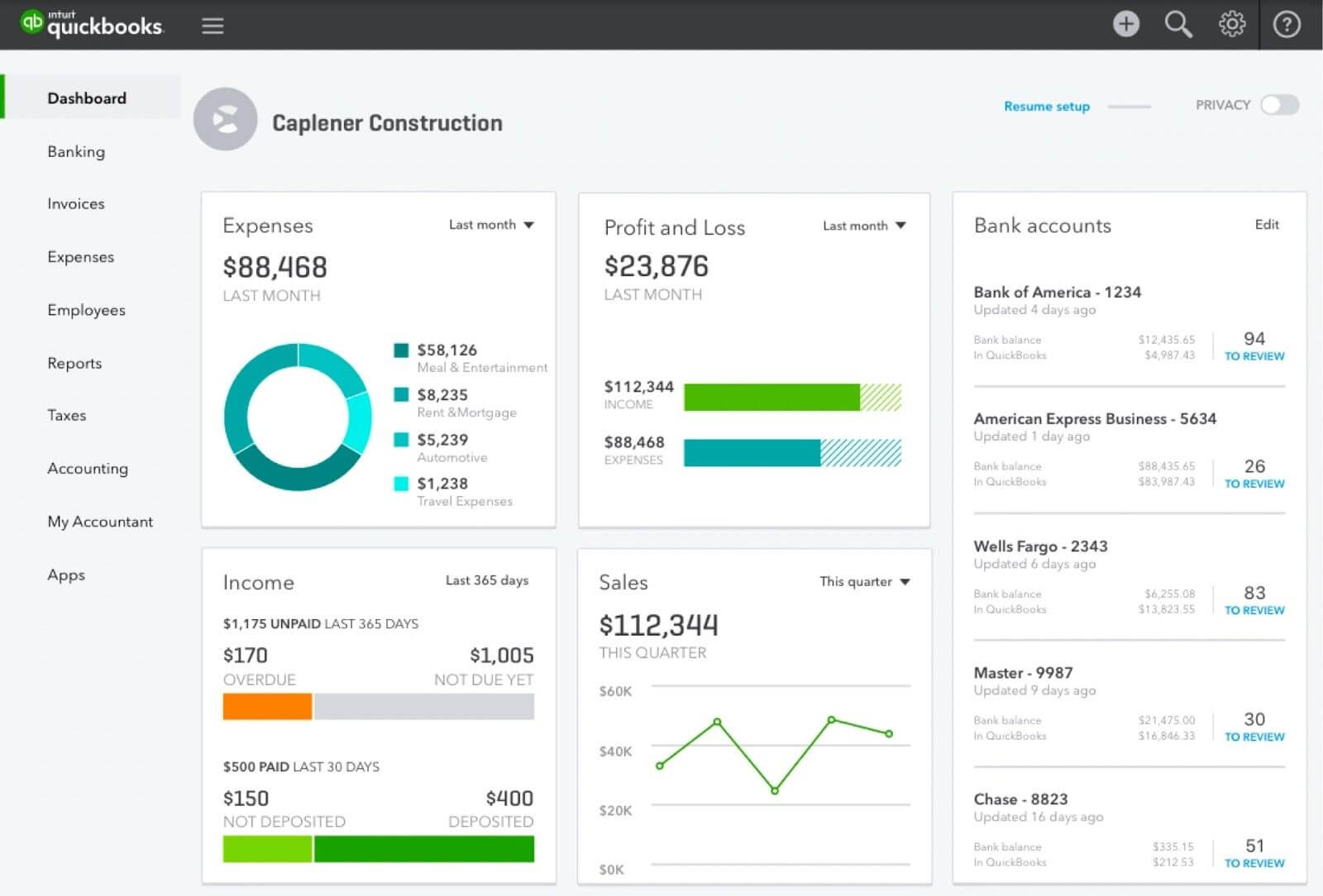

11. Set up your accounting systems

If your accounting system is set up correctly from the start—with future growth in mind—you’ll save yourself time and money long-term.

Many small business owners outsource their accounting to a bookkeeper or chartered accountant. While that can save you a lot of time, you still need access to tools that let you see how your finances are doing month-to-month.

Since cash flow is critical in the early days of starting a business, don’t launch without—at the very least—a cash flow spreadsheet in a tool like Excel as well as a balance sheet template.

You might also evaluate accounting software that automates this process and can help you visualise the money coming in versus your monthly outgoing payments.

Regardless of the option you choose, maintain an exhaustive record of all of your finances in one place. Every level of business has legal and tax obligations for record-keeping. Nailing down your bookkeeping from day one frees you up to work on growing your business.

12. Outsource essential functions early on

When starting a business, you might be tempted to do everything yourself to save money. But the time spent on tasks that aren’t your specialty can cost you money.

Prioritise your time towards the business objectives that will help you generate more revenue, faster.

Then, delegate or outsource tasks that aren’t your area of expertise (e.g., accounting, admin, or public relations). If you have the funds and legalities worked out, you can hire a few employees to share the workload.

It might be tough at first to trust other people with your business, but if you find great employees, you’ll question why you didn’t do it sooner.

If money is tight, but you still need help, you can enlist contractors or freelancers to help you cover areas where you aren’t strong. Managing your sanity is just as important as managing your time.

If you decide to hire someone instead of outsourcing …

13. Familiarise yourself with payroll taxes

Employee salaries require taxable amounts withheld from their payroll. You must treat certain contractor payments in a similar fashion. Speak with your accountant to ensure you meet all tax responsibilities.

Digital payroll services offer both self-service and full-service options. Some of the benefits of using payroll software include:

- You can set up and track employee benefits, superannuation, deductions, and garnishments

- Monitor employee payroll data and annual changes (e.g. bonuses and salary bumps)

- Have a digital process to automatically deposit your taxes to relevant governments

- Automatically add new employees to your payroll system

For more information on what’s involved in setting up and administering payroll, check out: 10 questions about single touch payroll . If you’d prefer, have a look at our Quickbook User Guides instead.

14. Build a basic web presence

If you don’t at least have a website and email address in today’s always-on, digital world, do you even exist?

Data from BrightLocal

To win new customers, a website must be included in your marketing strategy. Fortunately, you don’t have to spend a ton of money setting up your small business website. There are lots of affordable, easy-to-use options available.

When you have the time and resources, you can move on to adding social media profiles and consider other digital marketing tactics like paid ads, reviews, and search engine optimisation.

According to Inside Small Business , Australian businesses with a social media presence has reached record levels, with more than half of small businesses (51%) having a profile. Many are planning ever greater use and expenditure on social media in the next 12 months.

As your business grows, so too can your budget for building a stronger, more impactful digital marketing strategy.

15. Explore business partnerships

While we talked about reasons to go into partnership with others to start a business, we should also address partnering with other businesses for collective growth.

There are many different ways to form a partnership, like:

(1) Referrals and Revenue Share

Some work with partners to help them sell services in exchange for a commission or revenue share deal (e.g., one business gives another one a percentage of the sale). It’s very common if you have a small sales team and want to expand your efforts without hiring more full-time employees.

With referrals, you might offer a commission to a partner who helps introduce and assist you with closing a new prospective customer.

Revenue share is usually better for businesses that help a customer to use your product or service better. For example, software vendors have expert partners who might help a mutual customer to use the software in a more effective manner and, therefore, spend more time with the software vendor. The expert partner would, therefore, get a percentage of sales based on terms both parties would agree on.

(2) Joint Ventures

If you plan to, say build an office tower or make a movie, you might consider forming a joint venture with another business or group of businesses.

Let’s say you have all the equipment and staff to film the story, but want to add computer graphics in afterward. That’s where a partnership with another production business with that staff and those capabilities makes sense.

(3) Cross-promotions

If two businesses have similar target customers, it often makes sense to partner on a cross-promotion.

Spend some time thinking about whether there are businesses in your community that you can work with on a partnership deal. When approaching them:

- Be honest and clear about what you want and what’s in it for them

- Be patient and willing to negotiate to ensure both parties are happy with the deal

- Be willing to walk away if you can’t negotiate a fair and mutually profitable opportunity

Just like when you’re hiring employees, place trust at a premium. You can always ask their existing or past partners whether they were happy with a recent joint venture or cross-promotional experience.

Starting a business is the first step

This post outlines the necessary steps you must follow to launch a new business. Remember to start with your vision, research your opportunity, and record it all in a business plan or canvas.

It’s critical to understand and manage your startup costs and cash flow wisely. If you aren’t self-funded, find out which investment options make the most sense to your business.

Outsourcing or hiring employees who are experts in their field will free up your time to focus on what you do best and drive faster growth. You can also lean on business partners in your community for support and to collectively grow your customer base.

Always remember, fortune favours the bold. But it also smiles upon those who are prepared.

Source: Quickbooks